Dividend Yield vs. Dividend Growth: The 9-Minute Framework for Choosing the Right Income Strategy

High yield pays you more now. Dividend growth pays you more later. Here's a simple framework for deciding which fits your timeline, income needs, and portfolio goals — without overcomplicating the decision.

7/8/20269 min read

The best choice depends on when you need the money and how long you can let your investments grow. If you're retired and need income today, a stock paying 5% might make more sense than one paying 2%. But if you're decades from retirement, that 2% yield could grow to 10% or more on your original investment through consistent dividend increases. This is where dividend investing gets interesting—you're not just picking between two numbers, you're choosing between two paths to building wealth.

Understanding both dividend yield and dividend growth helps you make smarter choices about your dividend income strategy. Each approach affects your total return differently over time. The good news is you don't have to pick just one—many successful investors blend both strategies to match their current needs while still building for the future.

Key Takeaways

Dividend yield shows your current income while dividend growth shows how fast that income increases over time

Younger investors benefit more from growth strategies while retirees often need higher current yields

The most effective approach usually combines reasonable yield today with solid growth potential for the future

How Dividend Yield and Growth Work

Understanding Dividend Yield

Dividend yield shows the annual income you receive relative to what you paid for the stock. You calculate it by dividing the annual dividend payment by the current stock price, then multiplying by 100 to get a percentage.

If you buy a stock at $100 per share and it pays $4 in dividends each year, your dividend yield is 4%. This tells you that for every dollar you invest, you earn four cents annually in dividend income.

The yield changes as the stock price moves. If that same stock drops to $80, the yield rises to 5% ($4 ÷ $80). If the price climbs to $125, the yield falls to 3.2% ($4 ÷ $125). This means yield isn't fixed—it fluctuates with market conditions even when the dividend payout stays the same.

You can use a dividend calculator to project how different yields affect your income over time.

What Is Dividend Growth Rate?

The dividend growth rate measures how quickly a company increases its dividend payout over time. It's expressed as a percentage and typically calculated as the compound annual growth rate between two periods.

A company paying $1.00 per share this year and $1.10 next year has a 10% dividend growth rate. Companies that raise dividends consistently for 25+ years earn the title of Dividend Aristocrats.

Dividend growth stocks typically have lower starting yields but make up for it through regular increases. A stock yielding 2% today but growing its dividend at 8% annually will eventually produce more income than a 5% yielder with no growth. The catch is that you need time for this advantage to play out.

Core Differences and Calculation Methods

The key difference comes down to timing versus trajectory. Dividend yield answers "what am I earning right now?" while dividend growth rate answers "how fast is my income growing?"

Yield calculation: Annual dividend payment ÷ Current stock price × 100

Growth rate calculation: (Current year dividend - Previous year dividend) ÷ Previous year dividend × 100

High-yield stocks often sacrifice growth potential because they pay out more of their earnings now. Dividend growth stocks reinvest more capital back into the business, which can fund future dividend increases. Neither approach is automatically better—your choice depends on whether you need income today or want to build a larger income stream for later.

Comparing Investment Strategies

High-yield stocks and dividend growth strategies each offer distinct paths to building income. Understanding the advantages, risks, and key metrics of each approach helps you choose the strategy that matches your financial situation and timeline.

High-Yield: Advantages and Risks

High-yield stocks typically pay dividends of 4% or higher. You get immediate cash flow that shows up in your account right away. If you invest $50,000 at a 6% yield, that's $3,000 per year in dividend income from day one.

Advantages of high-yield stocks:

Immediate income without waiting years for growth

More shares purchased when reinvesting dividends

Larger cash flow from smaller portfolios

Strong returns in stable interest rate environments

Risks you need to watch:

Dividend cuts happen frequently with high-yield stocks

Interest rate changes hit these stocks harder

Slower price growth limits total returns

Dividend trap situations where high yields signal company problems

The payout ratio matters most here. When companies pay out 80-90% of earnings as dividends, they have little cushion during tough times. A single bad quarter can force a dividend cut that drops your income overnight.

Dividend Growth Approach: Pros and Cons

Dividend growth investing focuses on companies that raise their dividends consistently. Your starting yield might be just 2%, but growing dividends compound over time. A stock paying $1 per share today might pay $2 in seven years with 10% annual increases.

Pros of dividend growth strategies:

Protection against inflation through rising payments

Yield on cost increases dramatically over time

Better quality companies with stronger balance sheets

Higher total returns from both dividends and price appreciation

Cons to consider:

Low starting income requires patience

You need a large portfolio to generate meaningful cash initially

Premium valuations on popular dividend growers

Past dividend increases don't guarantee future ones

Dividend growth investing works best when you don't need the income now. Your initial 2% yield feels small, but reinvesting those growing dividends creates powerful compounding.

Crossover Point and Yield on Cost Explained

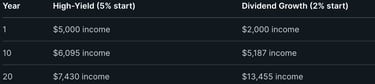

The crossover point is when dividend growth catches up to high-yield income. A portfolio starting at 2% yield with 10% annual dividend increases will surpass a 5% yield portfolio growing at 2% around year 12.

Yield on cost shows your actual return based on your original investment. If you bought a stock at $50 paying $1 annually (2% yield), and the dividend grows to $3 after 10 years, your yield on cost is now 6% on your original $50 investment. The current market yield might still show 2%, but you're earning 6% on your cost basis.

Example comparison:

Key Metrics: Payout Ratio, Dividend Increases, and Cuts

The payout ratio tells you what percentage of earnings goes to dividends. A 40% payout ratio means the company keeps 60% of profits for growth and safety. High-yield stocks often have 70-90% payout ratios, leaving little room for error.

Track dividend increases to spot healthy dividend growers. Look for companies raising dividends by 7-10% annually. Anything below 3% barely keeps pace with inflation. Above 15% might be unsustainable long-term.

Watch for warning signs of dividend cuts: declining revenue, falling profit margins, rising debt levels, and payout ratios above 100%. When companies pay more in dividends than they earn, cuts usually follow within 12-24 months.

Strong dividend growth companies typically maintain payout ratios between 30-60%, giving them flexibility to keep raising dividends even during downturns.

Building a Diversified Dividend Portfolio

A strong dividend portfolio balances different investment types and strategies to reduce risk while generating reliable income. You'll want to mix individual dividend-paying stocks with ETFs, consider your age and tax situation, and understand how different investment vehicles work together.

Role of Dividend Aristocrats, ETFs, and REITs

Dividend Aristocrats are companies that have increased their dividends for at least 25 consecutive years. These stocks give you proven business quality and dividend reliability. The Dividend Aristocrats index includes companies with strong free cash flow and stable earnings.

You can access these stocks through dividend ETFs like VYM (Vanguard High Dividend Yield), VIG (Vanguard Dividend Appreciation), or SCHD (Schwab U.S. Dividend Equity). Each ETF has a different focus. VYM targets high current yields, while VIG focuses on dividend growth. SCHD combines both yield and growth with strict quality screens.

REITs (Real Estate Investment Trusts) add real estate exposure to your dividend portfolio. They must distribute 90% of their taxable income as dividends, which creates high yields. REITs help diversify your income sources beyond traditional stocks.

JEPI (JPMorgan Equity Premium Income ETF) offers another approach. It combines dividend stocks with options strategies to generate monthly income. This can boost your passive income but works differently than traditional dividend investing.

Hybrid and Age-Based Approaches

Your dividend portfolio should match your age and income needs. Younger investors can focus more on dividend growth stocks that pay lower yields now but increase payments over time. This builds your future dividend income through compounding.

Older investors often need immediate income. You might weight your portfolio toward higher-yielding dividend ETFs and stocks. A common approach is the 50/50 split between stocks and bonds, but you can adjust based on your timeline.

A hybrid strategy combines high-yield and dividend growth investments. You might put 60% in dividend growth stocks or VIG, 30% in higher-yield options like SCHD or REITs, and 10% in income-focused investments like JEPI. This gives you current income plus growth potential.

Rebalance your portfolio annually to maintain your target allocation. As you age, gradually shift toward more stable, higher-yielding investments.

Tax Efficiency and Passive Income Considerations

Qualified dividends receive favorable tax treatment at 0%, 15%, or 20% rates depending on your income. Most dividends from U.S. companies and dividend ETFs like VYM, VIG, and SCHD qualify for these lower rates. This makes dividend income more tax-efficient than regular income.

REITs typically don't pay qualified dividends. Their distributions are taxed as ordinary income at your regular tax rate. Consider holding REITs in tax-advantaged accounts like IRAs to avoid higher taxes on your dividend income.

Income investing through dividend portfolios creates passive income streams that require minimal ongoing work. Once you build your portfolio, the dividend payments arrive automatically. Reinvesting these dividends in your earlier years accelerates your wealth building through compounding.

Track your dividend income separately from capital gains. This helps you understand your true passive income and plan for tax obligations. Use dividend ETFs for simplicity if managing individual stocks feels overwhelming.

Long-Term Wealth: Total Returns, Inflation, and Capital Growth

Building wealth through dividends requires looking beyond just the income you receive today. Total returns combine dividend income with capital appreciation, while growing dividends help your purchasing power keep pace with rising prices over time.

The Power of Compounding and Total Return

Total return measures both the dividends you receive and the increase in your stock's value. When you reinvest dividends, you buy more shares that generate additional dividends, creating a compounding effect.

A $10,000 investment in dividend growth stocks in 2005 grew to approximately $47,000 by 2024. The same amount in high-yield strategies reached only $32,500. This $14,500 difference shows how sustainable growth outperforms immediate income over two decades.

The compound annual growth rate (CAGR) captures this growth in a single percentage. Dividend growth stocks typically deliver higher CAGRs because companies that consistently raise dividends also tend to experience stock price appreciation. Your returns accelerate over time as both your share count and dividend rate per share increase.

Inflation Protection with Growing Dividends

Inflation erodes the purchasing power of fixed income streams. A stock paying $1,000 annually today will only buy $820 worth of goods in 10 years at 2% inflation.

Companies that raise dividends help you maintain and grow your real income. If a company increases its dividend by 7% annually, your income stream doubles every 10 years. This growth typically exceeds inflation rates, protecting your purchasing power.

The crossover point occurs when dividend growth stocks generate more annual income than high-yield stocks. While high-yield stocks pay more initially, growing dividends eventually surpass static higher yields. This crossover typically happens within 8-12 years depending on the growth rates.

Balancing Capital Appreciation and Income

Your investment mix should reflect your timeline and income needs. Younger investors benefit more from dividend growth because they have time for compounding to work. Retirees might prioritize current yield for immediate income.

Capital appreciation drives most long-term wealth creation. Stock price growth typically accounts for 60-70% of total returns over decades. Companies raising dividends signal financial strength, which often leads to higher stock valuations.

You can blend both approaches by holding dividend growth stocks for appreciation and some high-yield positions for current income. This balance lets you collect meaningful dividends today while building future income through growing payouts.

Conclusion

You don't have to choose just one strategy. Many investors blend both dividend yield and dividend growth to build a balanced portfolio that meets their needs.

If you need income right now, high-yield stocks can provide steady cash flow. Just watch out for companies that pay unsustainable dividends. Check their financial health before you invest.

If you're younger or don't need income immediately, dividend growth stocks might work better for you. These companies increase their payouts over time. Your income grows with them.

Think about your situation:

How much income do you need today?

What's your timeline for investing?

Can you handle some ups and downs in your portfolio?

Your answers will guide which approach makes sense for you. Some people start with growth stocks when they're young, then shift to high-yield stocks as they get closer to retirement.

Your next steps:

Review your current portfolio and goals

Decide how much immediate income you need

Both strategies can help you reach your financial goals. The key is picking the one that matches where you are in life. Don't wait to get started. The sooner you begin investing in dividend stocks, the more time your money has to grow and compound.

Contact

kbgholston445@gmail.com

© 2025. All rights reserved.