How Much Do You Need to Live on Dividends? Calculate Your Dividend Freedom Number in 15 Minutes

Living off dividend income is a real path to financial independence that many investors dream about. You can stop trading your time for money and let your investments work for you instead. The catch is knowing exactly how much you need to make it happen.

6/19/20267 min read

To live off dividends, you need to divide your annual income needs by your expected dividend yield, which typically means building a portfolio between $1 million and $3 million for most people. If you need $60,000 per year and earn a 2% dividend yield, you would need $3 million invested. If you can find investments with a 4% yield, that number drops to $1.5 million. The math is simple, but getting there takes planning.

The exciting news is that you have multiple ways to reach your goal. You can focus entirely on dividend income, or you can combine dividends with other withdrawal strategies to reduce how much you need to save. Your specific number depends on your lifestyle, your risk comfort level, and how you structure your investments.

Key Takeaways

Calculate your required portfolio size by dividing your annual expenses by your expected dividend yield

Building a dividend portfolio requires consistent investing and reinvesting dividends until you reach your target

You can reduce the amount needed by combining dividend income with strategic withdrawals using methods like the 4% rule

Calculating Your Dividend Income Requirement

To live on dividends, you need to know two numbers: how much cash you need each year and what dividend yield your portfolio will generate. These calculations determine the portfolio size you'll need to achieve dividend retirement.

Estimating Annual Expenses

Start with your current net pay and adjust it for retirement. Add Medicare premiums and out-of-pocket medical costs, which typically run $5,000 to $10,000 per year for most retirees. Subtract work expenses like commuting, professional clothes, and daily lunches.

Don't forget Social Security benefits. Visit the Social Security website to get your estimated monthly benefit. Subtract this amount from your total annual expenses to find your required portfolio income.

Include travel plans, hobbies, and bucket list activities in your budget. If you're paying off a mortgage or downsizing, subtract those savings. Add income taxes on withdrawals from traditional IRAs and 401(k)s. Most people need 70% to 80% of their pre-retirement income to maintain their lifestyle.

Determining Required Portfolio Size

Your required portfolio size depends on your annual expenses and target yield. The basic formula is simple: divide your annual expenses by your expected dividend yield. If you need $60,000 per year and target a 2% yield, you'll need a $3 million portfolio ($60,000 ÷ 0.02).

A living off dividends calculator can help you test different scenarios. The 4% rule offers a different approach. This rule suggests you can safely withdraw 4% of your portfolio annually for 30+ years. Using this method, a $1.5 million portfolio supports $60,000 in yearly retirement income.

The 4% rule lets you supplement dividend income by selling shares. This reduces your required portfolio size significantly compared to living on dividends alone.

Choosing a Target Dividend Yield

The S&P 500 currently yields about 1.35%, while the long-term average is 1.84%. Conservative dividend portfolios typically yield 2% to 3%. Higher yields (4-5% and above) mean a smaller required portfolio, but they often come with increased risk.

Common yield targets:

Conservative (1.5-2%): Blue-chip stocks, broad index funds

Moderate (2.5-3.5%): Dividend aristocrats, dividend-focused ETFs

Aggressive (4%+): REITs, high-yield ETFs, covered call funds

*I actually aim for much higher ones. If you're interested, check out this article ASAP!

A 3% yield on a $60,000 annual need requires a $2 million portfolio. A 4% yield drops that to $1.5 million. Balance your yield target with dividend safety and growth potential. Companies that pay sustainable dividends tend to increase payments over time, giving you inflation protection for your monthly dividend income.

Building a Reliable Dividend Portfolio

A strong dividend portfolio balances three critical elements: spreading risk across multiple investments, choosing stocks and funds with solid payment histories, and prioritizing companies that raise their dividends consistently over time.

Diversification Strategies

Your dividend portfolio needs protection from single-stock risk. Aim for 20-35 individual positions across different sectors to ensure one dividend cut won't derail your income stream.

Spread your investments across these key categories:

Dividend Aristocrats (30-40%): Companies with 25+ years of consecutive dividend increases

High-yield blue chips (20-25%): Established companies paying 4-6% yields

REITs (15-20%): Real estate investments offering monthly or quarterly payments

Dividend ETFs (15-25%): Funds like SCHD or HDV that provide instant diversification

Utilities and consumer staples (10-15%): Defensive sectors with stable cash flows

This mix gives you reliable income while limiting exposure to any single company or sector. If one position cuts its dividend, you'll only lose 3-5% of your total income instead of facing a major shortfall.

Selecting Dividend Stocks and Funds

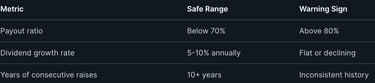

Quality matters more than yield when you're building a portfolio to live off dividends. Focus on companies with strong payout ratios below 80% and histories of raising dividends annually.

The dividend aristocrats list gives you a proven starting point. These companies have raised their dividends for at least 25 consecutive years. Names like Johnson & Johnson, Procter & Gamble, and Coca-Cola belong in most dividend portfolios.

Dividend ETFs offer instant diversification without requiring you to pick individual stocks. SCHD tracks high-quality dividend growers with an average yield around 3.5%. HDV focuses on high-yield stocks with strong financials.

Check these metrics before buying any dividend-paying stock:

Avoid chasing the highest yields. Stocks paying 10% or higher often can't sustain those payments and may cut dividends when business slows.

Optimizing for Dividend Growth and Sustainability

Dividend growth stocks protect you from inflation while building your future income. A company raising its dividend 7% annually will double your yield on cost in roughly 10 years.

Enable DRIP (dividend reinvestment plans) on all holdings until you need the income. This compounds your returns by automatically purchasing more shares with each dividend payment. A $500,000 portfolio earning 4% grows faster when those $20,000 annual dividends buy additional shares.

Focus on dividend sustainability by monitoring payout ratios quarterly. Companies paying out 40-60% of earnings as dividends have room to maintain payments during downturns and raise them during good times.

Dividend growth investing beats chasing high yields because your income increases every year. A stock yielding 3% today that raises dividends 8% annually will outpace a 5% yielder with flat payments within five years.

Track your portfolio yield separately from individual stock yields. Your blended yield shows the actual income you're generating across all positions. A mix of 3% aristocrats and 5% high-yield stocks might deliver a 4% portfolio yield that grows consistently.

Essential Considerations for Dividend Investors

Building a dividend portfolio goes beyond just picking high-yield stocks. You need to understand how taxes affect your returns, prepare for potential dividend cuts, and plan for additional income sources to create a reliable retirement strategy.

Dividend Taxation and Account Selection

A high dividend yield looks great on paper, but taxes can significantly reduce the income you actually keep.

Not all dividends are taxed the same way.

Qualified dividends receive favorable tax treatment and are typically taxed at long-term capital gains rates of 0%, 15%, or 20%, depending on your income.

Non-qualified dividends, on the other hand, are taxed as ordinary income and may face much higher tax rates.

Most dividends from regular stocks qualify for the lower tax rates if you meet the required holding period. However, investments such as REITs and MLPs often generate non-qualified dividends that can result in a larger tax bill.

Tax-advantaged accounts can help reduce this burden.

Traditional IRAs and 401(k)s allow dividends to grow tax-deferred until retirement.

Roth IRAs offer the greatest tax benefit since qualified withdrawals are completely tax-free.

Bottom Line

The best dividend investment isn't always the one with the highest yield—it's the one that leaves you with the most money after taxes.

Before investing, consider:

✅ Is the dividend qualified or non-qualified?

✅ Which account type should hold this investment?

✅ How much income will you actually keep after taxes?

A smart dividend strategy focuses on both income generation and tax efficiency, helping you maximize your long-term returns.

Managing Dividend Cuts and Sequence Risk

Companies can reduce or eliminate dividend payments at any time. A dividend cut usually triggers a stock price drop, hitting you twice.

Sequence of returns risk becomes critical when you rely on dividend income. If the market crashes right when you retire and companies slash dividends, your income drops exactly when you need it most. Diversification helps protect against this risk.

Funds like VYM and SCHD spread your investment across dozens or hundreds of dividend-paying companies. If one company cuts its dividend, the impact on your total income stays small.

Individual stocks like Realty Income have strong track records of consistent payments, but no dividend is guaranteed forever. Monitor your holdings monthly to catch problems early.

Supplementary Income Sources in Retirement

Living entirely on annual dividends requires a massive portfolio. Most retirees benefit from combining dividend income with other sources.

Social Security provides a foundation of guaranteed income. Treasury bonds offer reliable interest payments with zero default risk. Pensions add another stable income stream if available.

The 4% rule lets you safely withdraw from your portfolio by selling shares when needed, not just relying on dividends. This approach drastically reduces the portfolio size you need. A $75,000 annual income requirement needs $1.87 million at 4% versus $3.75 million at a 2% dividend yield.

Part-time work or consulting during early retirement can bridge any income gaps while letting your portfolio continue growing.

Conclusion

Living off dividends is completely achievable when you know the numbers. You need roughly 25 times your annual expenses at a 4% yield, or about 29 times at 3.5%. If you need $50,000 per year, that means building a portfolio between $1.25 and $1.67 million.

The best part? Your dividend income grows over time while your principal stays intact. You're not selling shares or watching your account balance shrink. Companies raise their dividends each year, giving you a built-in inflation hedge that beats traditional withdrawal strategies.

Start with these three steps:

Add a 20% buffer for unexpected costs

Divide your annual need by your target yield

That's your portfolio goal.

You don't need to hit this number overnight. Contributing $2,000 monthly for 20-25 years can get you there. Even starting with a $500/month dividend portfolio builds momentum and experience.

The journey takes planning and patience, but thousands of investors already live this reality. With dividend aristocrats, quality ETFs, and diversified positions, you can build reliable income that lasts forever. Your retirement doesn't have to mean selling stocks in down markets or worrying about running out of money.

Calculate your exact portfolio target today. Figure out your expenses, pick your yield target, and start building toward financial freedom through dividend income.

Contact

kbgholston445@gmail.com

© 2025. All rights reserved.