Compound Interest: How $200/Month at 25 Beats $600/Month at 35

Starting at 25 vs 35 changes everything. I'll show you the math: invest $24K total and retire with $590K, or invest $72K and get the same result. Time wins.

11/25/20258 min read

Most people understand that saving money matters, but fewer realize that when they start saving can be more important than how much they save. Compound interest is the process where money earns returns, and then those returns start earning returns too. This creates growth on top of growth, turning small regular investments into significant wealth over time.

Starting early with compound interest gives money more time to grow exponentially, meaning someone who invests less money at a younger age can end up with more wealth than someone who invests far more but starts later. Consider two people who each invest $200 per month with a 7% annual return. The person who starts at 25 and stops at 35 can end up with nearly the same retirement balance as someone who starts at 35 and invests until 65, despite contributing only one-third of the total amount. The difference is simply time!!

The math behind compound interest might sound complex, but the strategy is simple. Anyone can benefit from it by starting small, staying consistent, and letting time do the work. Even modest monthly contributions can grow into substantial savings when given decades to compound.

Key Takeaways

Compound interest lets money earn returns on both the original amount and accumulated gains over time

Starting to invest early matters more than the amount invested because time allows exponential growth

Regular contributions to investment accounts with automatic reinvestment maximize compound growth potential

※This article is going to contain some math along the way so my fellow hunters whose cup of tea ain't math, just bare with me and breeze over the math parts. I assure you that you'll have a better understanding at the end. Already bravo making it this far!! 😀

Understanding Compound Interest and Its Mechanics

Compound interest generates earnings on both the initial investment and the accumulated interest from previous periods. This creates a growth pattern that accelerates over time, building wealth faster than simple interest calculations where returns apply only to the original principal amount.

What Is Compound Interest?

Compound interest is the process of earning returns on both the original principal and the interest that accumulates over time. Unlike simple interest, which only calculates returns on the initial investment, compound interest creates a cycle where previous gains generate additional earnings.

The calculation involves three key components. The principal is the starting investment amount. The interest rate determines the percentage return each period. Time represents how long the money remains invested.

For example, a $1,000 investment at 5% annual interest earns $50 in year one. In year two, the calculation applies to $1,050 instead of the original $1,000. This means year two generates $52.50 in interest rather than another $50.

Financial accounts typically compound at different frequencies. Some compound annually, while others compound quarterly, monthly, or daily. More frequent compounding periods lead to higher total returns because interest starts earning its own interest sooner.

Understanding compounding is half the battle — understanding why we defer gratification is the other half.

📘The Psychology of Money nails that.

The Snowball Effect and Exponential Growth

The snowball effect describes how compound interest gains momentum as it grows. Early growth appears slow, but the rate accelerates significantly over longer periods as the base amount increases.

A $10,000 investment at 7% annual returns grows to approximately $19,672 after 10 years. After 20 years, it reaches $38,697. After 30 years, it climbs to $76,123. The investment nearly doubles in the first decade but multiplies almost four times in the second decade.

This pattern creates exponential growth rather than linear growth. The difference becomes dramatic over extended timeframes. Someone investing from age 25 to 35 and then stopping often accumulates more wealth by retirement than someone who invests the same annual amount from age 35 to 65.

Interest on Interest Explained

Interest on interest represents the core mechanism that makes compound interest powerful. Each compounding period adds new interest to the account balance, and this increased balance becomes the foundation for calculating the next period's interest.

The formula demonstrates this clearly: A = P(1 + r/n)^(nt), where A is the final amount, P is principal, r is annual interest rate, n is compounding frequency per year, and t is time in years.

Consider two scenarios with $5,000 invested at 6% for 25 years. With simple interest, the account grows to $12,500. With compound interest, it reaches $21,455. The $8,955 difference comes entirely from interest earned on accumulated interest rather than on the original principal.

The Critical Importance of Starting Early

Starting early in investing creates advantages that cannot be replicated by contributing larger amounts later in life. The time an investment has to grow matters more than the actual dollars invested, and even modest delays can cost investors tens of thousands in potential returns.

Time as the Most Valuable Ally

Time allows investments to compound repeatedly, creating exponential growth that accelerates in later years. An investor who starts at age 25 with $200 monthly contributions and earns a 7% annual return will accumulate approximately $525,000 by age 65.

The same investor starting at age 35 would need to contribute $440 monthly to reach the same goal. This difference shows why early investing beats larger contributions made later.

The final decade of a 40-year investment period generates more growth than the first two decades combined. Money invested early experiences multiple cycles of compounding, where returns generate their own returns year after year.

Annual Return and Rate of Return Impact

The rate of return directly determines how quickly investments double in value. At a 7% annual return, money doubles approximately every 10 years. At 10%, it doubles every 7 years.

Growth of $10,000 at Different Rates:

Higher returns paired with more time create dramatic differences in building wealth. A 3% difference in annual return over 40 years can result in hundreds of thousands of additional dollars.

The Cost of Delaying Investments

Every year an investor waits represents lost compounding opportunities that cannot be recovered. Delaying investment by just five years from age 25 to 30 costs approximately $150,000 in long-term wealth at a 7% return with $200 monthly contributions.

Waiting until age 40 to start requires tripling monthly contributions to match what someone starting at 25 would achieve. Most investors cannot afford to make up for lost time through larger contributions alone.

The penalty for waiting grows steeper with each passing year. An investor who delays from age 30 to 35 loses roughly $85,000 in potential growth, while delaying from 35 to 40 costs another $60,000.

Strategies to Maximize Compound Growth

Building wealth through compound interest requires more than just starting early. Smart investing habits, proper risk management, and automated systems help maximize returns over time.

Consistent Investing Habits

Regular contributions create the foundation for strong compound growth. Investors who add money consistently benefit from dollar-cost averaging, which means buying investments at different price points throughout the year. This approach reduces the impact of market volatility.

Setting up a monthly investment schedule helps remove emotions from investing decisions. Someone who invests $300 every month will build wealth faster than someone who tries to time the market. The stock market rewards consistency over perfection.

Even small amounts add up significantly over decades. An investor who contributes $150 monthly starting at age 25 can accumulate more wealth than someone who waits until age 35 to invest $300 monthly. Time matters more than the initial amount in personal finance.

Diversification and Managing Risk

Spreading investments across different asset types protects wealth while allowing compound growth to work. A balanced portfolio typically includes stocks, bonds, and other investments that respond differently to market conditions.

Key Asset Allocation Considerations:

Stocks offer higher growth potential but come with more risk

Bonds provide stability and regular income payments

Age-based adjustments help protect gains as retirement approaches

Younger investors can handle more stock market exposure because they have decades to recover from downturns. Someone in their 20s or 30s might hold 80-90% in stocks. Older investors often shift toward more bonds to preserve their accumulated wealth.

Diversification also means investing in different company sizes and sectors. This strategy prevents one bad investment from derailing overall compound growth.

Automated Contributions and Reinvestment

Automation removes the chance of skipping contributions or forgetting to reinvest earnings. Most employers offer automatic payroll deductions for retirement accounts. Brokerage firms also allow scheduled transfers from checking accounts.

Reinvesting dividends accelerates compound growth significantly. When dividend payments automatically purchase additional shares, those new shares generate their own dividends. This creates a powerful cycle of growth.

Setting up automatic increases to contribution amounts captures raises and bonuses. An investor who increases contributions by just 1% annually will accumulate substantially more wealth without feeling the impact on their budget.

Choosing the Right Investment Vehicles

The right investment accounts and funds can make compound interest work harder. Low-cost options protect returns from fees, while tax-advantaged accounts like 401(k)s accelerate growth over time.

Index Funds and Low-Cost Options

Index funds track entire market segments rather than trying to beat them. These funds automatically invest in hundreds or thousands of companies at once, which spreads out risk.

The main advantage is cost. Most index funds charge between 0.03% and 0.20% in annual fees. Actively managed funds often charge 1% or more. That difference matters because fees eat into compound interest over decades.

A low-cost index fund charging 0.10% versus an actively managed fund charging 1% can mean a difference of hundreds of thousands of dollars over 30-40 years. The money saved on fees stays invested and compounds.

Three common types include:

Total stock market index funds - Own pieces of nearly every public company

S&P 500 index funds - Track the 500 largest U.S. companies

International index funds - Provide exposure to companies outside the U.S.

Many investors build their entire strategy around these three fund types.

Understanding 401(k) and Retirement Accounts

A 401(k) offers two major benefits for compound interest. First, contributions reduce taxable income now. Second, money grows tax-free until withdrawal in retirement.

Many employers match contributions up to a certain percentage. This match is free money that immediately boosts investment returns. Someone who skips the match leaves that money on the table.

Traditional 401(k) accounts use pre-tax dollars and get taxed at withdrawal. Roth 401(k) accounts use after-tax dollars but withdrawals in retirement are tax-free. Younger workers often benefit more from Roth options since they have decades for tax-free growth.

Annual contribution limits for 2025 sit at $23,000 for workers under 50. Workers 50 and older can contribute an additional $7,500.

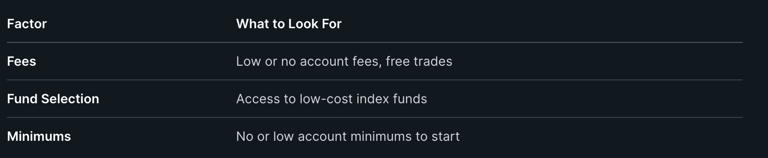

Evaluating Investment Platforms

Different platforms serve different needs. Employer-sponsored 401(k) plans come with limited fund choices but often include matching. Individual retirement accounts (IRAs) offer more flexibility in investment options.

Brokerage platforms like Vanguard, Fidelity, and Schwab offer low-cost index funds and minimal account fees. Most have eliminated trading commissions on stocks and ETFs. New investors should look for platforms with no account minimums and educational resources.

Robo-advisors automate investing by building and managing portfolios based on risk tolerance. They typically charge 0.25% to 0.50% annually. This option works well for hands-off investors but adds another fee layer on top of fund costs.

Investment platforms should be evaluated on three factors:

The best platform depends on whether someone invests through an employer plan or opens accounts independently. Both paths can lead to financial success when paired with consistent contributions and long time horizons.

BONUS READ literally!!

📚 Recommended Reading List for Beginners

If you want to start investing — and let compound interest work for you — these are the books I personally recommend:

Contact

kbgholston445@gmail.com

© 2025. All rights reserved.