Before Buying Any Monthly Dividend Stock, Read this First.

Monthly payouts can mask unsustainable yields, return-of-capital distributions, and debt levels that make cuts inevitable. Here's how to identify the warning signs before you buy — and which monthly dividend stocks experienced income investors avoid entirely.

6/16/202612 min read

The truth is that while monthly dividend stocks attract income-focused investors with their regular payouts, many hide problems beneath their attractive yields. Some companies use questionable tactics like returning your own money back to you while calling it "income," while others pile on debt or invest in risky ventures just to keep those monthly checks flowing. What looks like passive income on the surface might actually be a slow leak in your investment account.

Understanding these hidden dangers doesn't mean you need to avoid monthly dividend stocks entirely. It just means you need to be smarter about picking them. When you know what red flags to watch for and how to evaluate whether those monthly payments are actually sustainable, you can build a dividend investing strategy that works for you instead of against you.

Key Takeaways

Monthly dividend stocks offer convenient income but often carry higher risks like inflated yields and unsustainable payouts

Many monthly payers use risky strategies including leverage, return of capital, and lending to high-risk borrowers to maintain their distributions

Smart investors can benefit from monthly dividends by checking total returns, monitoring sustainability, and limiting exposure to riskier positions

Why Monthly Dividend Stocks Are So Popular (and Tempting)

Monthly dividend stocks attract investors with regular paychecks, faster growth through reinvestment, and easier budget planning. These features make them particularly appealing to retirees and anyone seeking passive income on a predictable schedule.

The Appeal of Consistent Cash Flow

Most dividend payers send you money four times a year. Monthly dividend stocks flip that script and deposit cash into your account every 30 days.

This creates a rhythm that feels more like a regular paycheck than an investment return. You get 12 chances each year to see money arrive instead of waiting months between payments.

For income-focused investors, this steady cash flow makes planning easier. You know when money will arrive, which helps you cover regular expenses without selling shares or dipping into savings.

Monthly dividends also provide psychological benefits. Seeing returns arrive regularly keeps you engaged with your investments and reminds you why you bought dividend stocks in the first place.

Faster Compounding With Reinvestment

The math behind dividend reinvestment works in your favor when payments arrive monthly. You put your returns back to work 12 times per year instead of four.

On a $100,000 investment earning 10%, monthly dividend reinvestment produces about $90 more in the first year compared to quarterly payments. By year ten, that gap grows to nearly $2,200.

Monthly vs. Quarterly Dividend Reinvestment (10% Yield on $100,000)

Monthly dividend stocks can look like a dream come true until the payment suddenly shrinks or disappears. Warning signs like sudden yield spikes, rising debt levels, and unsustainable payout ratios often reveal serious problems hiding beneath attractive distributions.

High Yields vs. Yield Traps

A genuinely high yield rewards you for taking on manageable risk. A yield trap punishes you for ignoring red flags.

The difference matters because yield traps appear when a stock's price crashes faster than its dividend. You might see a monthly payer offering 12% yield and think you've struck gold. But if that yield jumped from 6% to 12% because the share price got cut in half, you're looking at a trap until proven otherwise.

Watch these warning signs:

Yield spiked after a sharp price drop

Payout ratio above 100% (company pays more than it earns)

Negative free cash flow

History of previous dividend cuts

High-yield monthly dividend stocks often live in rate-sensitive or leverage-heavy sectors. When financing costs rise or credit conditions tighten, these monthly payers feel the pressure first. Your 10% yield means nothing if the company slashes the dividend by 50% next quarter.

Dividend Cuts: When the Paycheck Vanishes

Dividend cuts happen when companies can no longer afford their promised payments. Your monthly income stream dries up overnight.

Companies telegraph cuts through shrinking coverage ratios and eroding earnings. The dividend coverage ratio shows how many times earnings can cover the payout. Anything below 1.0 means trouble is brewing. The payout ratio tells a similar story—when it climbs above 80-90%, the dividend becomes fragile. Check out this article to understand more about these metrics!

Debt levels add another layer of danger. Heavily leveraged companies must choose between paying creditors and paying you. Guess who wins that fight? Sector-specific risk makes this worse. Mortgage REITs, for example, get squeezed when interest rates shift because their borrowing costs eat into distributable income.

You can't budget around vanishing dividends. One month you're collecting $500, the next month you're getting $200 or zero.

Return of Capital – Not as Sweet as It Sounds

One of the most misunderstood dividend concepts is Return of Capital (ROC).

At first glance, a distribution that lands in your account looks just like a dividend. But sometimes, part of that payment isn't investment income at all—it's simply your own money being returned to you.

Think of it this way:

A true dividend is paid from a company's profits or cash flow.

A return of capital is money paid back to investors that reduces the value of their original investment.

This matters because a high distribution yield can sometimes create the illusion that an investment is generating more income than it actually is.

For example, a fund might advertise a 10% yield. But if a large portion of those payments comes from ROC rather than earnings, the income may not be as sustainable as it appears.

Why Return of Capital Matters

ROC can create two important issues for investors:

1. More Tax Complexity

Return of capital reduces your cost basis in the investment. While this can defer taxes today, it may increase your capital gains taxes when you eventually sell.

2. Misleading Yield Numbers

A fund paying a large percentage of distributions through ROC may appear to have a high yield, even though the underlying income generation is much lower.

In other words, a headline yield doesn't always tell the whole story.

Is Return of Capital Always Bad?

Not necessarily.

Some investments—particularly certain REITs, closed-end funds, and income-focused funds—can generate legitimate ROC because of depreciation and other accounting adjustments.

In these cases, cash flow may remain healthy even if reported earnings appear lower.

The key is understanding why the ROC exists.

Bottom Line

Return of capital isn't automatically a red flag, but it should never be ignored.

Before investing in any high-yield fund or income investment, ask:

✅ How much of the distribution comes from actual earnings or cash flow?

✅ How much comes from return of capital?

✅ Is the payout sustainable over the long term?

A high yield is only valuable if it's backed by real income generation.

The best dividend investments don't just pay you today—they have the financial strength to keep paying you tomorrow.

Interest Rate Sensitivity and Market Downturns

Monthly dividend stocks don't operate in a vacuum. Interest rates and economic conditions can have a major impact on both their share prices and dividend sustainability.

When interest rates rise, investors often compare dividend stocks to safer alternatives like bonds and Treasury securities. For example, if Treasury yields increase from 2% to 5%, a stock yielding 7% may no longer look as attractive. This can lead to selling pressure and falling share prices.

Higher interest rates can also hurt companies directly. Businesses that rely heavily on debt may face higher borrowing costs, leaving less cash available to support dividend payments.

Economic downturns create another challenge.

Companies that only barely covered their dividends during strong economic periods may struggle when revenue and profits decline. In some cases, this can lead to dividend cuts.

Certain sectors are especially sensitive:

REITs depend on property values and occupancy rates.

Business Development Companies (BDCs) rely on healthy lending activity and low loan defaults.

Bottom Line

A high dividend yield doesn't guarantee a safe investment.

Always consider the bigger picture:

✅ Can the company handle higher interest rates?

✅ Is the dividend well-covered during weaker economic conditions?

✅ Does the business have a history of maintaining payouts during downturns?

The strongest dividend stocks aren't just built for good times—they're built to survive bad ones too.

You can't control when downturns hit, but you can avoid dividend payers with shaky fundamentals, excessive debt, and sector-specific risks that multiply during recessions.

How to Pick Monthly Dividend Stocks Without Tripping Over Your Own Wallet

Spotting Sustainable Payouts and Avoiding the Classic Mistakes

A 15% yield looks amazing until the company cuts its dividend in half and the stock price drops 30%. You just lost money chasing yield.

Check dividend history going back at least five years. Consistent dividend payments matter more than high yields. If a company has raised or maintained its dividend through multiple economic cycles, that's a green flag. Monthly cuts, freezes, or wild fluctuations? Red flags everywhere.

Watch out for "return of capital" distributions. This isn't real dividend income—it's the company giving you back your own money. Your tax forms will show this, and it means the business can't generate enough cash to actually pay you. Dividend investors who ignore this wake up one day owning a shrinking investment.

Calculate the sustainability yourself. Take annual dividend payout amounts and compare them to the company's earnings or cash flow. If they're paying out 120% of what they earn, basic math says that can't last. You want companies keeping some profits to grow and handle emergencies.

Famous Monthly Payers (and a Few Ominous Tales)

Realty Income (O) is the poster child of monthly dividends. They own over 13,000 commercial properties and collect rent from tenants like Walgreens and Dollar General. Their dividend history spans decades with annual increases. That's what sustainability looks like in real life.

Main Street Capital takes a different approach. They lend money to middle-market companies and collect monthly interest payments. Those payments fund your dividends. The risk? If borrowers default during economic downturns, your dividend income could drop.

Then there are cautionary tales. Some closed-end funds with 12% yields looked great in 2025 but cut distributions by 40% in early 2026 when their underlying assets dropped in value. Their yields were artificially inflated through leverage—borrowing money to buy more investments. When markets turned, the debt crushed them.

Dividend Aristocrats don't usually pay monthly, but studying them teaches you what quality looks like. They've raised dividends for 25+ consecutive years because they manage cash flow like professionals, not gamblers.

Start with Dividend ETFs for Monthly Income

If picking individual stocks makes your head hurt, monthly dividend ETFs do the homework for you. These funds own dozens or hundreds of dividend-paying stocks and handle the research, rebalancing, and risk management.

You get instant diversification without buying 20 different companies yourself. One ETF might hold REITs, BDCs, preferred stocks, and utilities all in one package. Your monthly dividend income arrives on schedule while professional managers watch the underlying holdings.

The trade-off is fees. ETFs charge expense ratios, usually between 0.3% and 1.5% annually. That eats into your returns compared to owning stocks directly. But for beginners or hands-off investors, the convenience beats the cost.

Look for ETFs with consistent track records and reasonable expense ratios under 0.75%. Check what they actually own—some "dividend" funds are packed with risky junk yielding 15% that won't last. You want boring, stable holdings that prioritize consistent dividend payments over flashy yields.

Compounding returns work better when you reinvest those monthly payments automatically. Most brokers let you set this up for free with ETFs. Your dividends buy more shares, which generate more dividends, which buy more shares. Over years, this snowball effect builds wealth while you sleep—assuming you picked solid investments that don't blow up.

Balancing Rewards and Risks for Smarter Dividend Investing

Your dividend income strategy needs guard rails, not just gas pedals. Smart investors build portfolios that balance high-yield temptations with stable, long-term performers while accounting for the tax realities that can quietly eat into returns.

Building a Resilient, Income-Focused Portfolio

You shouldn't put all your eggs in the monthly dividend basket, no matter how attractive those payouts look. A resilient portfolio mixes monthly dividend stocks with quarterly dividend stocks from established companies.

Mix safer options with riskier plays:

Cap your high-yield monthly positions at 15-20% of your total portfolio

Include dividend aristocrats that have raised payments for 25+ years

Add index funds for diversification beyond income-focused investments

Balance REITs and BDCs with traditional blue-chip dividend payers

Monthly dividend payments offer predictable income that matches your bills. But quarterly payers often come from more stable companies with lower dividend yields and better growth potential.

Your compounding returns benefit from diversification too. When one sector struggles, others can maintain steady dividend income. This approach protects you from the risk of concentrated positions in high-yield stocks that might cut distributions during economic downturns.

Mitigating Tax Surprises and Planning for the Long Term

Your tax bill matters as much as your dividend yield when calculating real returns. Monthly dividend stocks create more taxable events each year, and many produce nonqualified dividends taxed at higher ordinary income rates.

Smart tax strategies include:

Holding REITs and BDCs in tax-advantaged retirement accounts

Keeping qualified dividend stocks in taxable accounts for lower tax rates

Tracking all 12 monthly payments carefully for accurate tax reporting

Consulting a tax professional before building large positions

You need to calculate after-tax returns to see your true progress toward financial independence. A 10% yield taxed at 37% leaves you with 6.3%, while a 6% qualified dividend yield taxed at 15% gives you 5.1%. The gap narrows considerably.

Monthly dividend payments in a Roth IRA grow tax-free forever. This setup maximizes your compounding advantage while eliminating the headache of tracking dozens of small distributions each year.

Conclusion

Monthly dividend stocks aren't the income villain some investors make them out to be, but they're not your retirement fairy godmother either. You need to treat them like that friend who's really fun at parties but sometimes makes questionable decisions.

The real trick is knowing what you're getting into before you buy. Check the total return, not just that shiny yield that caught your eye. Make sure the company isn't just borrowing money or returning your own capital to keep up appearances.

Here's your game plan:

Keep monthly dividend stocks to a reasonable slice of your portfolio (not the whole pie)

Mix them with safer blue-chip stocks and ETFs

Set clear rules for when you'll sell

Actually check in on them regularly instead of pretending they don't exist

The convenience of monthly income is real. Your bills don't wait for quarterly dividends, and that extra compounding adds up over time. But convenience doesn't mean you can ignore the risks that come with higher yields.

Don't invest in something just because it pays you every month. Invest because the business makes sense, the dividend is sustainable, and it fits your overall strategy.

You're not locked into one approach forever. Start with positions you understand, learn as you go, and adjust when things change. The stocks that work for you today might not be the same ones you need in five years.

Now go build that income stream, but keep your eyes open while you do it.

A dividend reinvestment plan lets you automatically put this money back into more shares. The extra compounding power adds up faster than most people expect.

Convenience for Retirement and Budgeting

Your monthly bills arrive on a schedule. Rent, utilities, insurance, and groceries all demand payment at regular intervals throughout the month.

Monthly dividend payers align your passive income with these expenses. You receive money when you need it most, which reduces the need to maintain large cash reserves.

Retirees particularly value this feature. Instead of receiving a large dividend payment once per quarter and managing it carefully, you get smaller amounts that match your spending patterns.

This approach also reduces the temptation to spend dividend income all at once. Smaller, frequent payments encourage better financial discipline and smoother cash management.

Where Monthly Dividend Payers Come From

Most monthly dividend stocks fall into specific categories. Real estate investment trusts (REITs) lead the pack because they collect rent payments monthly and must distribute 90% of taxable income to shareholders.

Business development companies (BDCs) also pay monthly for similar reasons. These companies provide financing to smaller businesses and receive regular loan payments. Like REITs, BDCs must pay out 90% of their income.

Closed-end funds round out the list. These actively managed funds hold various assets and target investors who want high-yield monthly income. The underlying investments might not produce monthly returns, but the fund distributes payments on that schedule anyway.

Some utilities and specialized companies also pay monthly dividends, though they're less common. The key factor is predictable revenue that supports regular distributions without straining the business.

Unmasking the Risks: Red Flags and Yield Traps

Choosing monthly dividend stocks requires checking balance sheets, spreading risk across sectors, verifying payout sustainability, learning from real companies' track records, and considering ETFs as a safer starting point.

Evaluating Balance Sheets and Cash Flow

Your first job is figuring out if a company actually has the money to pay you every month. Look at the balance sheet like you're a suspicious accountant with trust issues.

Free cash flow is your best friend here. It shows the actual cash a company generates after paying its bills and buying equipment. If a company's dividend payments eat up more than 90% of its free cash flow, you're looking at a ticking time bomb. The business has no cushion for bad months or emergencies.

Check the dividend coverage ratio by dividing earnings or cash flow by total dividend payments. You want this number above 1.2 at minimum. Anything below 1.0 means the company is paying out more than it earns, which is like buying a new car when you can't afford groceries.

Main Street Capital (MAIN) is a business development company that shows how this works. They report detailed cash flow statements each quarter. Their dividend payments come from interest they collect on loans to smaller businesses. When those borrowers pay on time, Main Street has cash to send your way.

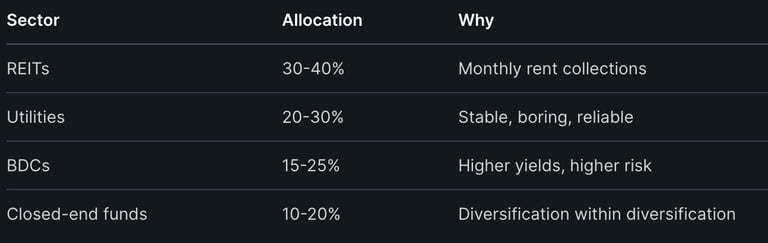

The Power of Diversification and Defensive Sectors

Don't put all your eggs in one monthly-paying basket. Your portfolio needs variety, or one bad sector will wreck your whole income stream.

Utilities are the boring superheroes of dividend investing. People pay their electric bills even during recessions. Companies like this provide steady income because their cash flow doesn't swing wildly. Mix these with REITs, BDCs, and maybe some income funds to spread your risk.

Defensive sectors include healthcare, consumer staples, and yes, those utilities. These businesses sell things people need regardless of the economy. Your monthly dividend income gets more reliable when you're not betting everything on one industry.

Here's a simple mix to consider:

Contact

kbgholston445@gmail.com

© 2025. All rights reserved.