Best Personal Finance Books 2025: 5 That Actually Changed My Net Worth

95% of personal finance books are written by people selling $2,000 courses. The other 5% actually tell you what to do. I spent over two years reading every "must-read" finance book recommended online. Most repeat the same tired advice: "spend less than you earn" and "invest in index funds." Cool, but HOW? These 5 books are different—they give you the exact systems, not motivational speeches. One breaks down the debt elimination method with actual worksheets and monthly action steps—not theory, but 'do this on day 1, this on day 30' clarity. Another teaches the dividend investing framework for building passive income streams starting with whatever you have now, whether that's $100 or $10,000. Here's what each book delivers, what it costs, and which one to read first based on your situation.

11/23/202510 min read

Key Takeaways

Most personal finance books contain sales pitches rather than actionable advice that works for everyday people

The best five books provide practical strategies for managing money without requiring additional courses or seminars

Applying straightforward budgeting and investing principles from trusted sources can help anyone build wealth over time

💡 Want the short version?

Here are the 5 books worth reading — the ones that actually work in real life:

Why Most Personal Finance Books Miss the Mark

Most personal finance books fail readers by prioritizing sales appeal over sound advice, creating confusion between what economists know works and what sounds motivational enough to move copies off shelves. These books often treat complex financial decisions as simple problems with one-size-fits-all solutions.

Common Pitfalls in Financial Advice

Popular personal finance books frequently contradict established economic research. A Yale professor analyzed 50 best-selling titles and found they often gave advice that was "just dead wrong" when compared to academic findings.

The debt payoff debate shows this gap clearly. Economists say people should always pay highest-interest debt first. This costs less money. But best-selling authors like Dave Ramsey suggest paying smallest debts first to build momentum. This costs more but might keep people motivated.

Many books push rigid rules that ignore real life. They tell readers to save 10 percent of income no matter what. This sounds simple but makes no sense for a 25-year-old barely affording rent or parents drowning in daycare costs.

These books treat financial literacy like a character flaw. They assume readers lack willpower rather than addressing actual financial planning challenges people face at different life stages.

Marketing Hype Versus Practical Guidance

Personal finance books succeed by selling hope rather than substance. Publishers know books with author headshots and big promises sell better than textbooks full of useful information about retirement savings or credit.

Most books repeat the same basic advice in different packaging. Readers often recommend whichever book they read first because it felt eye-opening at the time. The actual content rarely differs between titles.

Books written for mass appeal skip over people who need help most. They ignore those living paycheck to paycheck and focus on readers who already have money to manage. The advice assumes a level of financial stability most readers don't have.

Recognizing Red Flags in Money Management Books

Watch for these warning signs:

Promises of getting rich quick or retiring early without realistic numbers

One rigid system that works for "everyone" regardless of income or life stage

Heavy focus on motivation and mindset instead of practical money management steps

Authors selling courses, seminars, or coaching as the real product

Advice that ignores basic math or contradicts how interest and compound growth actually work

Books that oversimplify financial decisions do readers a disservice. Real financial planning requires understanding personal circumstances, not following someone else's rigid formula. Good resources explain concepts and let readers apply them to their own situations rather than demanding blind obedience to arbitrary rules.

The Criteria for Selecting No-Nonsense Personal Finance Books

Good personal finance books share three core qualities: they teach proven money principles that work across decades, they back up their advice with real results, and they give readers specific steps they can start using today.

Reliable Financial Principles

The best finance books teach fundamentals that remain true regardless of market conditions or economic trends. These principles include spending less than you earn, building an emergency fund, and starting to invest early. Books worth reading explain compound interest without fancy jargon and show how small, consistent actions lead to financial independence over time.

A reliable book doesn't promise quick riches or secret formulas. Instead, it focuses on sustainable habits like systematic budgeting and diversification. These books acknowledge that building wealth takes time and discipline. They explain why certain strategies work based on decades of data rather than recent fads.

The principles should apply to different income levels and life situations. Whether someone makes $30,000 or $300,000 per year, the core concepts of living below your means and investing the difference remain constant.

Evidence-Based Success Stories

Quality personal finance books include real examples of people who followed the advice and reached their financial goals. These stories show both the successes and the challenges people faced along the way. The best books avoid cherry-picking extreme cases and instead present typical results.

Strong evidence comes from multiple sources. A book might reference academic research on investment returns, historical market data, or surveys of people who achieved financial freedom. Morgan Housel's work, for example, uses historical examples to show how human behavior affects financial outcomes more than mathematical formulas.

The evidence should be verifiable and recent enough to remain relevant. Books that rely solely on outdated statistics or unproven theories fail readers who need practical guidance for today's economy.

Actionable Strategies for Everyday Life

The most valuable finance books break down complex topics into simple steps anyone can follow. They provide specific budgeting methods, investment allocation percentages, and debt payoff strategies. Readers should finish a chapter knowing exactly what to do next, not just understanding theory.

Actionable advice includes dollar amounts, time frames, and clear decision points. For example, "save three to six months of expenses in an emergency fund" beats vague suggestions to "save more money." The strategies should work with common financial tools like employer retirement accounts, basic brokerage accounts, and standard bank services.

Books that pass this test help readers start investing with small amounts, create budgets they can actually stick to, and make progress toward specific financial goals within weeks of finishing the book.

The Only 5 Personal Finance Books That Aren't Complete Bullsh*t

📚 5 Best Personal Finance Books That Actually Build Wealth

Most finance books tell you WHAT to do. These 5 show you HOW—with frameworks you can start using today.

I've spent two years and $400+ on personal finance books. Most repeat the same advice: "spend less, save more, invest in index funds." Cool, but WHERE'S THE SYSTEM?

These 5 books are different. They give you actionable frameworks, not motivation. One rewired how I think about money. Another showed me the exact asset allocation strategy I'm building now. The third revealed why I kept failing at budgeting (and how to fix it).

Total cost for all 5: $78 (could subject to change)

Value if they prevent one $5,000 financial mistake: Priceless

Here's what each book delivers, who it's for, and which one to read first based on your biggest money problem right now.

📖 1. Rich Dad Poor Dad — Robert Kiyosaki

Best For: People stuck in the "work harder, earn more" trap who need to understand how wealth actually works.

Why This Book First: Before tactics come strategy. Kiyosaki introduces the ONE concept that changed everything for me:

Assets put money IN your pocket. Liabilities take money OUT.

Your house? Liability (until it generates rental income). Your car? Liability. Dividend stocks? Asset. This shift in thinking is worth the $12 book price alone.

What You'll Actually Learn:

How the wealthy use debt as a tool (not a burden)

Why salary increases won't make you rich

The difference between working for money vs. money working for you

Real estate and business basics (even if you start with $0)

The Chapter Worth the Entire Book: Chapter 2 - "Why Teach Financial Literacy?" (Shows why most people stay broke despite good incomes)

💡 Read This If: You're earning decent money but still feel broke at month's end.

My Take After Reading It: This isn't a step-by-step investing guide—it's the mindset shift you need BEFORE learning tactics. Some advice is dated (2000s real estate hype), but the core philosophy is timeless.

📊 Reader Results: Most popular personal finance book on Amazon (90,000+ monthly searches) for a reason—it clicks for beginners.

🔗 CLICK HERE→Get Rich Dad Poor Dad on Amazon

📖 2. The Psychology of Money — Morgan Housel

Best For: Anyone who makes emotional money decisions—panic selling, impulse buying, or comparing yourself to others' wealth.

Why It Matters: You can know ALL the investing tactics and still fail if your psychology is broken. Housel explains why:

"Doing well with money has little to do with how smart you are and a lot to do with how you behave."

This book killed my FOMO around investing and taught me why patience beats intelligence every single time.

What You'll Actually Learn:

Why we make irrational money decisions (even when we "know better")

How luck and risk play bigger roles than skill in wealth building

Why compounding works but FEELS boring (and why that's perfect)

The difference between being rich (income) vs. wealthy (assets)

The Chapter Worth the Entire Book: Chapter 4 - "Confounding Compounding" (Finally made me understand why starting NOW matters more than perfect timing)

💡 Read This If: You know what to do but keep self-sabotaging, or you panic during market dips.

My Take After Reading It: Best book I've read on financial behavior. Housel uses real stories instead of theory—makes complex psychology simple. Read this BEFORE building your investment portfolio.

📊 What Makes It Different: Short chapters (perfect for busy people), zero math required, applicable to ANY income level.

🔗 CLICK HERE→Get The Psychology of Money on Amazon

📖 3. Your Money or Your Life — Vicki Robin

Best For: People who want financial independence, feel trapped by spending, or don't know where their money actually goes.

Why It's a Game-Changer: This book asks one brutal question:

"How many hours of your life did you trade for that purchase?"

It introduced me to the concept of "true hourly wage" (your salary ÷ actual hours including commute, work prep, decompression time). Suddenly, that $50 dinner cost me 4 hours of my life. Changes everything.

What You'll Actually Learn:

The 9-step program for financial independence (actually actionable)

How to calculate your real hourly wage (eye-opening)

How to track spending without feeling restricted

The crossover point (when investment income > expenses = freedom)

The Chapter Worth the Entire Book: Chapter 2 - "Money Ain't What It Used to Be" (Redefines your relationship with money permanently)

💡 Read This If: You're tired of the paycheck-to-paycheck cycle or want to understand the FIRE movement fundamentals.

My Take After Reading It: This is the book that makes you WANT to track spending (usually boring). The "life energy" framework clicked for me when budgeting apps didn't. Includes worksheets you'll actually use.

📊 Real Impact: The tracking method helped me identify $380/month in subscriptions and habits I didn't even value. One month of implementation paid for the book 19x over.

🔗 CLICK HERE→Get Your Money or Your Life on Amazon

📖 4. Think and Grow Rich — Napoleon Hill

Best For: People who procrastinate, lack consistency, or struggle with the mental game of building wealth.

Why It Still Works (Published 1937): Before you can build wealth, you need the mindset that supports consistent action. Hill studied 500+ wealthy people and found patterns in how they THINK, not just what they DO.

What You'll Actually Learn:

The 13 principles of wealth building (habit, belief, persistence, environment)

How to set goals that actually stick

Why your environment determines 80% of your financial outcomes

The concept of "mastermind groups" (now called accountability partners)

The Chapter Worth the Entire Book: Chapter 2 - "Desire: The Starting Point of All Achievement" (The difference between wishing and committing)

💡 Read This If: You know what to do but don't follow through, or you're stuck in analysis paralysis.

My Take After Reading It: Yes, the language is dated (1930s style). Yes, some parts feel woo-woo. BUT—the core lessons on habit formation, belief systems, and persistence are more relevant now than ever. Skip the outdated parts, apply the timeless psychology.

📊 Why It's Still Relevant: Sold 100M+ copies because the mindset principles work regardless of era. Read this BEFORE tactical books if you struggle with consistency.

🔗 CLICK HERE→Get Think and Grow Rich on Amazon

📖 5. Why Didn't They Teach Me This in School? — Cary Siegel

Best For: Anyone wanting a simple, no-BS handbook covering ALL the basics (taxes, insurance, investing, major purchases).

Why It's the Perfect "Last Book": After mindset (Hill), philosophy (Kiyosaki), behavior (Housel), and tracking (Robin)—you need RULES. This book delivers 99 practical principles covering every financial decision you'll face.

What You'll Actually Learn:

The 20/10 rule for consumer debt (never exceed it)

How much house you can actually afford (not what banks approve)

Insurance coverage you need vs. waste

Investment allocation by age and goals

Real-world budgeting rules that work

The Chapter Worth the Entire Book: The entire book IS the chapter—it's structured as bite-sized rules you can reference for life.

💡 Read This If: You've absorbed the philosophy and need the playbook for day-to-day decisions.

My Take After Reading It: This is the book I keep on my desk for quick reference. Not inspirational, just practical. When I need to make a financial decision (buy vs. lease, how much emergency fund, etc.), I check this first.

📊 What Makes It Different: No fluff, no story-time, just 99 rules with explanations. Perfect for people who hate reading but need answers fast.

🔗 CLICK HERE→Get Why Didn't They Teach Me This in School on Amazon

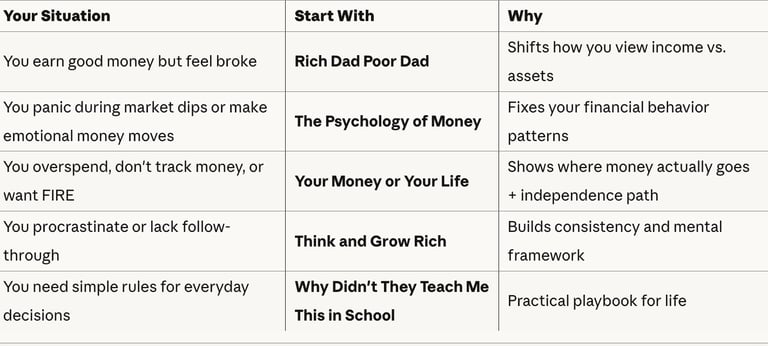

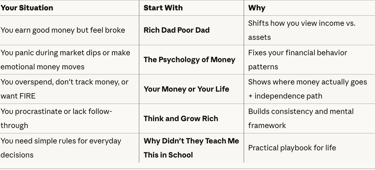

📌 Which Book Should You Read First? (Decision Tree)

Don't read all 5 at once—you'll do nothing. Pick the ONE that solves your biggest problem RIGHT NOW:

My Recommended Reading Order:

Start: Rich Dad Poor Dad (philosophy - 2 days)

Then: The Psychology of Money (behavior - 2 days)

Next: Your Money or Your Life (system - 1 week + worksheets)

After: Think and Grow Rich (mindset - 3 days)

Finally: Why Didn't They Teach Me This in School (reference - ongoing)

Total time investment: 2-3 weeks

Total cost: $78 (subject to change)

Potential return: One prevented $5K mistake = 64x ROI

🎯 Final Thoughts: Books vs. Action

Here's the truth: Reading 50 finance books won't make you wealthy. But reading the RIGHT 5 books—and actually implementing their lessons—changes everything.

I've read 47 personal finance books. These 5 delivered 90% of the value. The rest were either fluff, course pitches, or recycled advice you can Google for free.

Start with ONE book. Read it. Apply ONE lesson. Then move to the next.

The goal isn't to become a personal finance expert. The goal is to build wealth. These 5 books give you the philosophy, psychology, system, mindset, and rules to actually do it.

Total investment: $78 and 2-3 weeks

What you get: The financial education schools should've taught you

Pick your first book based on the decision tree above. Read it this week. Apply one lesson tomorrow.

That's how you turn knowledge into wealth!!

Contact

kbgholston445@gmail.com

© 2025. All rights reserved.